As global regulators struggle to keep pace with crypto adoption, tax authorities are turning to new data and digital tools to detect hidden gains. The UK’s latest crackdown highlights how Know Your Transaction (KYT) technology may be able to bridge the visibility gap between on-chain activity and apparent tax payer declarations.

The Global Crypto Tax Challenge

Tax compliance remains one of the most complex, and often misunderstood aspects of crypto regulation. Across the world, governments are tightening their frameworks, and yet law enforcement appears to lag behind blockchain innovation.

Jurisdictions such as the US, Japan and EU have clear reporting requirements for gains through crypto, but the pseudonymous and borderless nature of digital assets still allows users to move funds between wallets, exchanges and DeFi platforms, with somewhat little oversight.

A 2023 study from the Becker Friedman Institute estimated that crypto tax evasion costs governments billions globally. In fact, a letter from US Senators to the US Treasury explicitly warned that ‘tax evaders and the crypto intermediaries [...] siphon off billions of dollars a year from the US government’.

Thus, a growing enforcement gap is created: millions of taxpayers may be underreporting or omitting crypto income, and this could simply be due to the difficulty for authorities to trace crypto transactions.

UK’s ‘Nudge Letter’ Efforts

As a response, the UK’s tax authority HMRC issued over 65,000 ‘nudge letters’ to individuals suspected of failing to declare crypto-related gains. This figure is more than double the previous year. Data from crypto exchanges was acquired in order to identify the potential cases of tax avoidance or evasion. This campaign is similar to India’s efforts. Indian tax authorities are currently using data from Binance to pursue hundreds of suspected crypto tax evaders.

This course of action also mirrors efforts made by the US Internal Revenue Service in 2019. The authority originally sent out 10,000 letters, as well as five different Virtual Currency Compliance campaigns to address tax compliance issues, and inform taxpayers. The Financial Times reports that recently, the UK Tax Office has been working closely with the IRS, to obtain and analyse data on crypto transactions in efforts to close the gap.

This effort actually also aligns with HMRC’s Crypto Asset Reporting Framework (CARF) that the UK intends to implement in 2026. Once live, CARF will require exchanges and wallet providers to automatically share transactions and ownership data with tax authorities.

According to KPMG, CARF will raise over £315 million in additional tax revenue during its first phase.

Naturally, exchanges and wallet providers could benefit from KYT, utilising transaction monitoring to share transaction data with the authorities.

However, for the authorities themselves, given the expected influx of new data sources, the upcoming challenge is an analytical one. How can millions of on-chain records be processed, interpreted and acted upon?

What can KYT bring to Tax Enforcement?

KYT, or ‘Know your Transaction’ is the compliance backbone already relied upon by exchanges, payment processors and virtual asset service providers (VASPs) to monitor crypto activity in real time.

It continuously scans transactions for risk, detecting patterns linked to money laundering, sanctions evasion, or illicit behaviour.

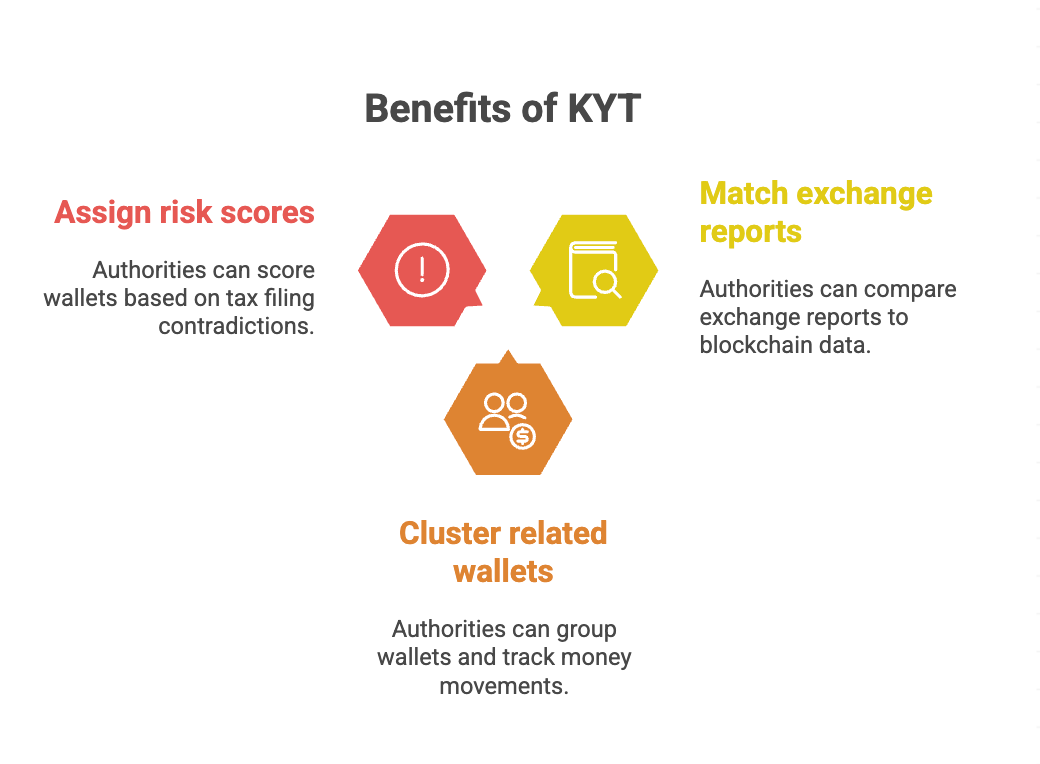

For tax authorities, KYT could do something similar, but focused on tax evasion indicators as opposed to purely AML benchmarks. By integrating KYT analytics with data from exchanges, authorities could:

- Match exchange reports to blockchain flows, automatically identifying gaps between reported and actual transfers

- Cluster related wallets and trace fund movements, revealing when taxpayers move assets to self-custody or off-shore exchanges

- Assign risk scores to wallets, based on involvement in events that contradict tax filings

This would transform tax oversight from a reactive audit process into a continuous and data-driven compliance network.

The Future of Crypto Tax Compliance

The crypto tax gap is not exclusively a UK problem, as the Becker Friedman study highlighted. From the US to Australia and the European Commission, regulators are all asking the same question - how can you enforce tax compliance in a pseudonymous financial system?

It appears the answer lies in the use of transaction intelligence, like Know Your Transaction, to fulfil the ever-growing requirements of new Tax Compliance frameworks, like CARF. As the digital economy evolves, tax authorities that can integrate these tools will move from chasing non-compliance years later to detecting it in near-real time.

Crypto tax evasion is not a niche issue, and does not exist in a vacuum. It directly affects financial integrity and public trust.

As regulators prepare for a new era of crypto reporting, KYT could become the missing link between blockchain transparency and effective tax enforcement.

All research content and accompanying reports are provided for informational purposes only and should not be relied upon as professional advice. Accessing these materials does not create any professional relationship or duty of care. Readers are encouraged to consult appropriately qualified professionals for guidance. We uphold the highest standards of accuracy in all the information we provide. For any questions or feedback, please contact us at contact@nominis.io.

.png)

.png)

.jpg)